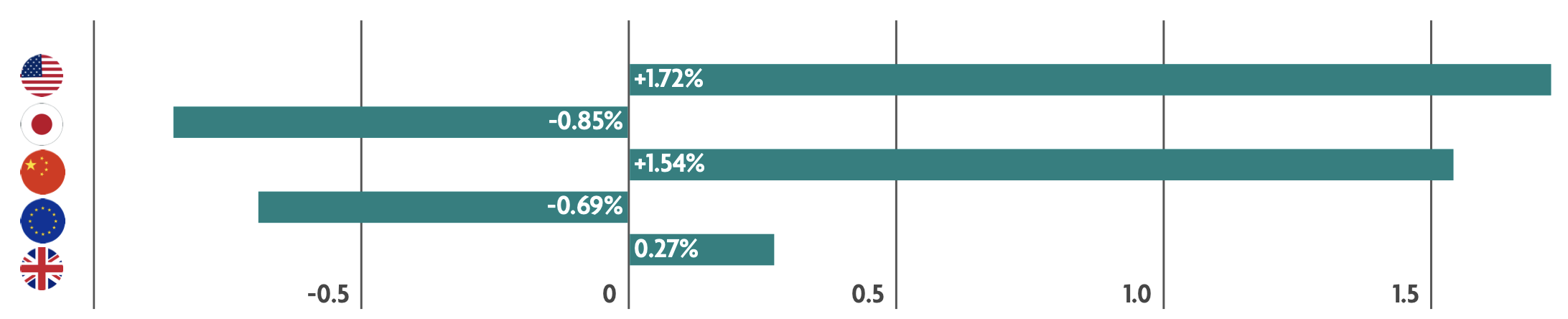

Weekly Market Update – 7 July 2025: S&P Hits New Highs as Global Markets Diverge

A muted week for markets in terms of news, with mixed returns across the world during the week. In the US, we saw markets reach new highs, whilst in Japan the lack of progress in trade negotiations weighed on sentiment. Data on China’s economy paints a mixed picture. As inflation settles in Europe, the European Central Bank considers what next for interest rates. And in the UK, the housing market appears to be recovering following a momentary downturn.

US: S&P 500 reaches a new high

It was a relatively quiet week in terms of news, but much of the focus during the week centred around the progress of the Trump administration’s reconciliation bill, which was narrowly passed by the Senate on Tuesday and by the House of Representatives on Thursday afternoon. Trade-related headlines also continued to flow during the week, with President Donald Trump announcing a trade deal with Vietnam on Wednesday and making comments around negotiations with several other trade partners ahead of the upcoming July 9 tariff deadline, when the 90-day pause on reciprocal tariffs is expected to end. On the economic data front, job growth remained resilient during the month of June, and unemployment moved slightly lower. Activity in the manufacturing sector contracted for the fourth consecutive month in June, but the services sector returned to growth after contracting in May.

Japan: Progress in U.S.-Japan trade negotiations stalling, weighing on sentiment.

Investors’ focus was on the latest developments in the bilateral trade negotiations between the U.S. and Japan - in the absence of an agreement, a 24% reciprocal tariff on Japanese imports is due to be reinstated by the U.S. on 9th July. Elsewhere, business sentiment amongst Japan’s big manufacturers unexpectedly improved in the three months to June, but these manufacturers expect business confidence to fall over the next few months. Investors also looked ahead to Japan’s Upper House election on 20th July, which is expected to lead to some political uncertainty in the short term.

China: mixed snapshot of China’s economy

A handful of indicators offered a mixed snapshot of China’s economy. On one hand, the manufacturing sector saw a small improvement in business activity during June, which comes after the U.S. and China agreed in May on a 90-day pause in their tariff war leading to a temporary rebound in trade. On the other hand, the services side of the economy remained under pressure. Activity in the services sector dropped from the month of May and has fallen to the lowest level since last September. Furthermore, a gauge of employment fell for the third time in the past four months as service providers remained cautious about hiring.

Europe: Interest rate cut pause on the horizon?

Headline annual inflation in the eurozone ticked up to the European Central Bank’s (ECB) 2.0% target in June after hitting an eight-month low of 1.9% in May. Meanwhile, the labour market in the eurozone area remained strong. Christine Lagarde, the President of the ECB reacted to the inflation data saying that the ECB’s target had been reached – this possibly indicates that we are approaching a pause in the central bank’s interest rate cuts this year.

UK: Housing market recovering?

The UK Nationwide house price index fell 0.8% in June after rising 0.4% in May. What this means, is if compared year over year, home prices are now 2.1% higher. Nationwide said it expected prices to rise over the summer, when demand for houses is usually strongest. Meanwhile, data from the Bank of England suggested that the housing market was recovering from a momentary downturn that occurred after the end of a tax break in April.

Lets Keep in Touch

To learn more about personal finance, sign up to our monthly newsletter

Thank you for subscribing!

Have a great day!

Content provided by Omnis Investments.

*Source: Bloomberg. All performance measured in local currency.

Issued by Omnis Investments Limited. This update reflects Omnis’ view at the time of writing and is subject to change. The document is for informational purposes only and is not investment advice. We recommend you discuss any investment decisions with your financial adviser. Omnis is unable to provide investment advice. Every effort is made to ensure the accuracy of the information, but no assurance or warranties are given. Past performance should not be considered as a guide to future performance.

The Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC are authorised Investment Companies with Variable Capital. The authorised corporate director of the Omnis Managed Investments ICVC and the Omnis Portfolio Investments ICVC is Omnis Investments Limited (Registered Address: Auckland House, Lydiard Fields, Swindon SN5 8UB) which is authorised and regulated by the Financial Conduct Authority.